Naomi quoted George Reisman as follows: Thus, in the pre-capitalist economy, only workers receive incomes and there is no money capital. But all the incomes which the workers receive are profits, and none are wages. In the sequence C-M-C, everything is "surplus value"—one-hundred percent of the sales receipts and an infinite percentage of the zero money capital. In the sequence M-C- M?, a smaller proportion of the incomes is "surplus value"—in degree that M is large relative to M?.

And replied: Reisman confuses or does not understand the distinction between profit and surplus value. He thinks that they are the same thing, but they're not. Surplus value is what is left over after the economy has produced everything it needs to reproduce itself. The economy obviously does not produce ONLY what is necessary for reproducing itself, (since otherwise it would never grow). It also produces a little more. This is what Smith calls the "natural recompense" and what Marx calls the "surplus value". Profit is just total revenue minus total cost. True, profit is total revenue minus total cost. The reason Reisman says that in the pre-capitalist economy, all income is profit is that the workers have no money costs to deduct from their sales receipts. So their entire income is profit; it's also surplus value, because, according to Marx, surplus value "is the excess of value produced by the labor of workers over the wages they are paid." (Oxford English Dictionary). Since in a pre-capitalist economy, there are no wages, as there are no capitalists (no employers), the worker's entire income is surplus value. Since wages are zero, the value produced in excess of wages is 100%. It is also profit, since profit is the excess of receipts from the sale of products over the money costs of producing them, which in a pre-capitalist economy is also zero, as there are no money costs of production. Note that it is possible for profit to be zero even though the surplus value is non-zero. If some workers produce 500 bushels of wheat, and they need only 400 to feed themselves, then the surplus value is 100 bushels of wheat. If they sell the extra bushels for 10 coins a piece, then their profit is 1000 coins. However, if they don't sell the extra bushels, and just consume them or store them away, then their profit is zero, but nonetheless, the surplus value is still 100 bushels of wheat. Remember, surplus value is the excess of value produced (in this case, 500 bushels of wheat) over the wages the workers are paid. Since they aren't paid any wages, their surplus value is 100%. Even if they sell only 100 of the 500 bushels, their profit (of 1000 coins) is also 100%, since (again) profit is the excess of sales receipts over the money costs of production, and in this case, there are no money costs of production. So 1000 coins minus zero money costs equals 100% profit. This is why Reisman says that in a pre-capitalist economy, all money income is profit. The rest of his argument is that Smith and Marx are wrong. Wages are not the primary form of income in production. Profits are. In order for wages to exist in production, it is first necessary that there be capitalists. The emergence of capitalists does not bring into existence the phenomenon of profit. Profit exists prior to their emergence. The emergence of capitalists brings into existence the phenomena of wages and money costs of production. Accordingly, the profits which exist in a capitalist society are not a deduction from what was originally wages. On the contrary, the wages and the other money costs are a deduction from sales receipts—from what was originally all profit. The effect of capitalism is to create wages and to reduce profits relative to sales receipts. The more economically capitalistic the economy—the more the buying in order to sell relative to the sales receipts, the higher are wages and the lower are profits relative to sales receipts.

Neither Smith nor Marx are saying that wages (as we understand the term today) are the "primary" form of income in production. What they are saying is that "in that rude state of things" (to use Smith's terms) or under "primitive communism" (to use Marx's), the laborers retain the entirety of the surplus value (not profit). Well, "in the rude state of things," surplus value is profit, since profit is total revenue minus total cost and there are no money costs. Remember, in a pre-capitalist economy, it's C-M-C, in which a worker produces a commodity C, sells it for money M, and then buys other commodities C. What they refered to as the wage was the "natural wage", the amount of value that a laborer receives in order to sustain himself. Then, under the "natural wage," surplus value would be the excess of what the laborer produces over what he needs for bare subsistance, correct? What they receive in wages under capitalism is called the "market wage", and it consists of the natural wage plus some portion of the surplus value (this portion, at least according to Marx, is determined by political forces and not economic forces). The rest of the surplus value goes to the capitalist. This distinction between the "natural wage" and the "market wage" is confusing, given Marx's concept of "surplus value" as "the excess of value produced by the labor of workers over the wages they are paid." My understanding is that, according to Marx, his concept of surplus value applied to capitalism, but you're now saying that under capitalism, the "market wage" includes "some portion of the surplus value." Doesn't this contradict his definition of 'surplus value', none of which is included in the workers wages under capitalism? Also Merlin noted, "Not one word about supply and demand." To which you replied, Because those concepts are completely unnecessary, and also, nonsensical. They're neither unnecessary nor nonsensical, as they explain why some workers under capitalism receive very high wages, far above subsistence level, while other workers receive much lower wages. Money wages are determined by the supply and demand for labor. If the demand is high for a particular skill or talent, but the supply of workers possessing that skill or talent is low, then the wages tend to be high, because employers compete for the very valuable but relatively scarce labor, and in so doing bid up its wages. We see this in the high salaries of CEOs and professional athletes. Conversely, if the supply of workers possessing a particular skill or ability is high (because most people possess it) relative to demand, then the wages for those workers tend to be low. We see this in the wages of fast food workers and day laborers.

|

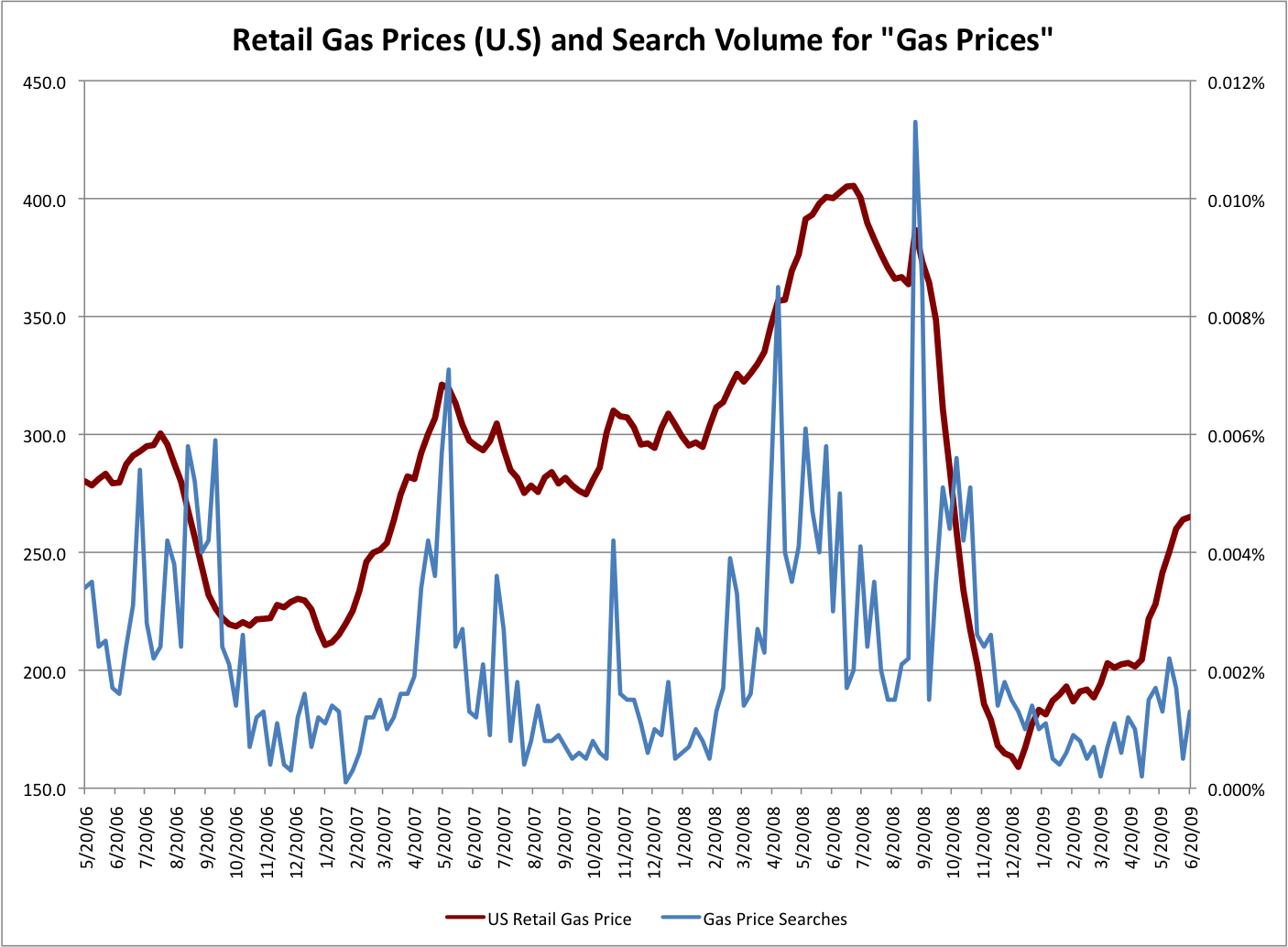

Please explain to us relying only on the LTV the phenomena of (a) gasoline prices rising just before holidays and falling shortly after and (2) many, many retail prices falling shortly after Christmas.

Please explain to us relying only on the LTV the phenomena of (a) gasoline prices rising just before holidays and falling shortly after and (2) many, many retail prices falling shortly after Christmas.